Health services have enormous potential for mitigating many of the global health problems that afflict much of the world’s population. However, it is a sad fact that all the heroic ambitions for improving global health must confront the prosaic reality of finding the necessary financial resources. The remorseless logic of accountancy requires that the funds needed to provide services must be raised somehow, and there are regrettably few alternatives as to how that can be achieved.

Yet some countries do seem to be able to finance their health services far more painlessly than others. So there are many lessons to be learned about how best to fund health services, especially in low income settings.

As well as providing the necessary resources, many of the decisions made about financing are a key determinant of the nature and performance of any health system. The sort of questions to be addressed by finance policymakers include:

- Who should pay for health services?

- How much should they pay?

- What services should be subsidized?

- How should the providers of those health services be reimbursed?

The answers to these questions will in very large part determine the scope and nature of services that are provided, who receives those services, and the extent to which poor or sick people are exposed to impoverishing health-related payments. In short, financing is a key determinant of the efficiency and fairness of the health system.

Health Spending and National Income

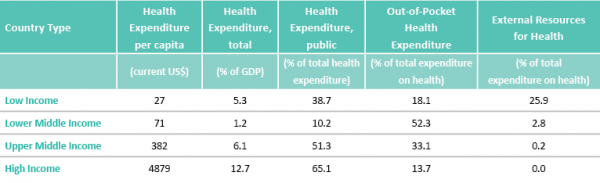

It is first worth noting the magnitude of the financing task. Health expenditure per annum amounts to just $27 per person in low income countries, compared to $4,879 in high income settings. This underlines the most basic difficulty confronting any efforts to address global health concerns: the profound scarcity of resources in low income settings. And resources available even in middle income countries are pitiful when compared with the high income countries. Of course one reason for this is the relatively low proportion of national income committed to health services in low and middle countries - see column two of the table.

Paradoxically, for many countries it is only as national income increases that it is possible to increase the proportion of the economy devoted to health, even though the most pressing health needs are clearly at low income levels. A number of reasons account for the inability of low income countries to prioritize health, such as the presence of even more pressing spending priorities, the reluctance of health service providers to operate in low income settings, and concerns about the quality and efficiency of services.

It can be argued that protection from health-related financial catastrophe is one of the great triumphs of twentieth century social policy in developed nations

Columns three and four demonstrate another clear trend: as national income increases, the proportion of health expenditure funded from public sources (such as taxation or mandatory social insurance) increases, and the reliance on out-of-pocket spending declines. Indeed it can be argued that protection from health-related financial catastrophe is one of the great triumphs of twentieth century social policy in developed nations.

Reducing the reliance on direct user charges for health services yields enormous benefits for citizens, in particular the very poorest. First there is the immediate benefit that households are protected from the financial hardship (and sometimes catastrophe) associated with paying for healthcare. But the reduced financial barriers to access to care have also been shown to yield major benefits in terms of population health, worker productivity and the broader prosperity of society.

As a result, development of improved protection from the financial consequences of illness has become a policy priority for many countries. It is noteworthy that the topic chosen for the World Health Report 2010 was ‘universal health coverage’: the notion that citizens should have access to needed health services of sufficient quality to be effective, without entailing financial hardship.

Universal Health Coverage

In general, with the notable exception (so far) of the United States, citizens in developed countries enjoy very high levels of coverage. Access to most needed services is readily available, and the associated fees are generally modest. This is achieved through systems of universal health insurance, such as the mandatory social health insurance used in countries like the Netherlands and Germany, or state funded health insurance of the sort provided in Scandinavia and the United Kingdom.

These insurance arrangements secure affordable coverage by charging citizens according to their ability to pay (usually income levels), rather than their levels of sickness. They therefore implicitly make a very large financial redistribution from the major financial contributors (the rich, the young and the healthy) to the major recipients of care (the poor, the old and the sick).

Of course low income countries do not have the capacity to purchase a full range of health services for the whole population, and they therefore tend to provide lower levels of coverage than their richer counterparts.

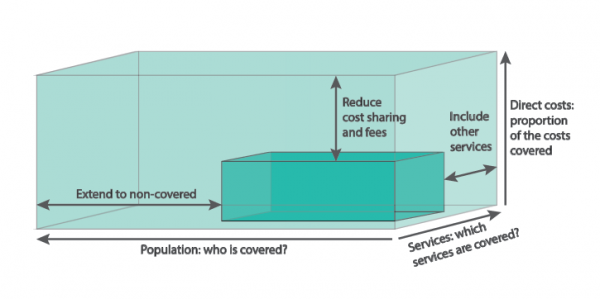

WHO characterize the level of coverage as a box in which the ‘breadth’ of coverage indicates the proportion of the population enjoying insurance protection from public insurance funds, the ‘depth’ of coverage indicates the range of services covered (how comprehensive is the benefits package?), and the ‘height’ of coverage indicates the degree of protection from user fees (because even if a service is nominally funded by the insurance arrangements, the patient might still have to pay a charge).

The size of the blue box indicates schematically the level of coverage enjoyed by the population; to attain a higher level of coverage requires either higher levels of funding or improved levels of efficiency.

Having secured a certain level of ‘pooled’ funding for health funding, policymakers must then decide which people to insure, which services to include in the national ‘benefits package’, and how much to charge people for access to those services. Of course, many would like to see all citizens being insured for all services, with no charges for securing access.

However, this position ignores the harsh reality that the size of the blue box in the figure shown overleaf is decidedly finite. Simple arithmetic makes it infeasible for all people to be insured for all services with zero price for access. In short, the policy problem is to make the difficult financing choices illustrated above.

Taxation for Health

One strategy for improving coverage is to increase the volume of pooled funding for health services (the size of the blue box). A number of approaches can be envisaged to this end, but perhaps the most fundamental is to develop trusted insurance arrangements.

Contributors to the health insurance pools can then feel confident that they and their dependants will be able to secure access to needed services when they suffer ill-health in the future. Such trust is a fundamental requirement for the efficient operation of any insurance arrangement, whether run by governments, non-governmental organizations, or the private sector.

It has been become evident that – to be effective – health insurance arrangements must be mandatory, covering a large population, with contributions graduated so as to reflect ability to pay. In effect they must take the form of taxation. A small number of low and middle income countries, such as South Africa and Uruguay, have historically placed a high reliance on voluntary private health insurance, at least for higher income citizens.

This protects those who can afford such insurance from health-related income shocks. In the same way, experiments with small-scale ‘community based insurance’ can be useful in demonstrating in low income settings the benefits of insurance (relative to user fees). However, if enrolment is voluntary, voluntary community based schemes tend to attract sicker citizens, and will therefore not be financially sustainable unless they can make a transition to a universal system of mandatory health insurance. Furthermore, of course, such voluntary insurance is much more readily accessible to richer citizens. In short, to achieve the goals of health improvement, financial protection and equity, universal health coverage requires a move towards some form of tax-based funding.

Health insurance arrangements must be mandatory, covering a large population, with contributions graduated so as to reflect ability to pay

Yet there is obviously a shortage of the necessary taxable capacity to fund health services in low income settings. The table underlines the heavy reliance of low income health systems on ‘external’ funds, in the form of foreign aid. Since 1990 the volume of health aid has increased from $6 billion to $28 billion (at constant 2009 prices), and it now accounts for 25% of all health expenditure in low income countries, from sources such as individual donor countries, non-governmental organizations and foundations including the Bill and Melinda Gates Foundation, and international agencies such as the Global Fund, the World Bank and the WHO.

Whilst these funds are a welcome supplement to the country’s own resources, they often create added complication for policymakers, especially when (as is usual) they are tied to specific health programmes, rather than a general supplement to a country’s own financial resources.

Also, researchers are becoming concerned that donor funds may to some extent displace funds for health services that would otherwise have been raised by the country itself, rather than to supplement planned health spending. For example, one effect of donor funds may be to allow a country to spend its own health resources on other sectors, such as government education programmes or even reduced taxation.

Another way to increase the effective size of the blue box is to increase the efficiency of the health services that it funds. There are manifest inefficiencies in almost all settings, so in principle this should offer a fruitful way of making pooled funds go further. There is increasing recognition that health system inefficiency is immoral, because it wastes money and therefore denies treatment for people in need.

There are some hopeful signs, such as the increased use of telemedicine and better information on provider performance. However, there is no simple solution to driving out inefficiency, with a few percentage points a year likely to be the best that can be achieved in most situations. The reduction of waste will therefore usually require a long term commitment of energy and leadership.

Although increased revenue and enhanced efficiency can yield some leeway for policy makers, it is likely that – in most settings – the hard choices will remain of who will receive coverage, for what services, and at what level of price. Economists have traditionally championed cost-effectiveness analysis as the basis for making many of those choices. The idea of cost-effectiveness analysis is that the services to be covered should offer the biggest health gains for the limited money available.

This gives rise to some tough solutions, and may have to be adapted somewhat to protect the poorest people. However it is difficult to envisage a fairer or more transparent way of spending the limited health budget, and it is reassuring to see adoption of such methods in global initiatives such as WHO CHOICE (CHOosing Interventions that are Cost Effective) and the Disease Control Priorities Project.

Governance, Transparency and Accountability

The financing of health services is a basic pillar of every health system, and there is increasing recognition that it has a fundamental influence on the health of the population and their broader prosperity.

There are some very hopeful signs, such as moves towards genuinely universal coverage in countries such as Thailand and China, and careful specification of the benefits package in line with a nation’s ability to pay, as in Chile. Approaches towards improved efficiency are less well developed, but there are some hints of success, such as Rwanda’s success in implementing a system of paying providers in line with performance.

In summary, financing arrangements are a key determinant of health system performance. Future priorities will always include the following:

- The creation of trusted agencies to oversee the collection and spending of pooled health service funds;

- Clear statements of what services are to be funded from the pooled funds;

- Development of incentives for providers and citizens to encourage appropriate utilization and greater efficiency;

- The active measurement of performance so that insurers, providers, clinicians and governments can all be properly held to account for the results achieved.

There are active debates about how these are to be best achieved. For example, some promote the merits of provider competition, whilst others champion a public service ethos. No approach towards health system design has been shown to be unambiguously superior, so it is likely that the emphasis will to some extent depend on local circumstances. However, any system of finance will fail without the universal requirements of good governance, transparency, and proper accountability.